Body

The Financial Accountability in Research (FAIR) model is a new approach to indirect cost recovery, or facilities and administrative (F&A) costs, developed by the research community in collaboration with government leaders. The FAIR model:

- Eliminates “F&A” terminology and the associated rate proposal preparation by creating new trackable costing categories that are easier to understand

- Accommodates all types and sizes of institutions

- Increases accountability and transparency via explicit costing of key research support

- Clarifies institutional use of reimbursed funds by tracking costs in specific and allowable categories

- Aligns project costs with the type of work being performed

- Accounts for geographic cost differentials

- Funds government-mandated regulatory compliance

- Aligns funding structure more closely with that allowed by private foundations by treating more items as direct costs

- Will require changes to Uniform Guidance (2 CFR Part 200) and policies

Process for Adopting a New Model

1. What organizations are leading the development of a new model?

Ten national organizations comprise the Joint Associations Group on Indirect Costs (JAG):

- Association of American Universities (AAU)

- Association of Public and Land-grant Universities (APLU)

- Association of American Medical Colleges (AAMC)

- American Council on Education (ACE)

- Association of Independent Research Institutes (AIRI)

- COGR

- National Association of College and University Business Officers (NACUBO)

- National Association of Independent Colleges and Universities (NAICU)

- American Association of State Colleges and Universities (AASCU)

- Science Philanthropy Alliance (SPA) – SPA contributed ideas and staff time to the JAG effort, but as a matter of policy does not speak for its partner organizations, so takes no formal position on the FAIR Model

The initiative was announced on April 8, 2025, as a community-based effort to develop potential replacement models for the funding of indirect costs on federal research grants.

2. Why undertake this effort now?

The JAG organizations have undertaken this effort to help shape a new indirect costs policy that is fair, transparent, and durable. The FAIR model responds to Members of Congress who have called on the community to put forward a new simple and transparent model to pay for the essential costs necessary to perform research for the federal government on behalf of the American people.

The FAIR model represents an alternative to the arbitrary, across-the-board 15 percent cap on indirect cost rates, which has been proposed by the NIH, NSF, DOE and DOD. While the proposed caps have not been implemented due to ongoing litigation and legislation, if implemented, they would substantially degrade America’s research and innovation enterprise and global competitiveness.

3. How was the subject matter expert (SME) team assembled?

The SME team was assembled by the JAG and includes individuals who have broad knowledge of direct and indirect costs, federal agency policies and procedures, cost accounting, private sector and National Laboratory funding models, philanthropic funding of research, and research administration. They represent public and private academic research institutions of varying types and sizes, independent research institutes, academic medical centers, and hospitals. The team also includes representatives from private foundations and industry. The SME team was assembled to be representative of the breadth of non-governmental organizations subject to 2 CFR Part 200 cost principles (public/private and large/small institutions, HBCUs, EPSCoR state universities, nonprofit research organizations, etc.).

4. What has the Joint Associations Group on Indirect Costs (JAG) done to engage the research community?

The JAG has engaged the research community and received input in several ways:

- JAG organizations have convened and discussed ideas and models with their members and internal working groups. Feedback has been collected and shared through the JAG organizations to the SME team.

- The JAG hosted two public town halls in May to introduce the effort and take questions and comments. More than 1,000 individuals from the research community participated in each town hall, and they submitted more than 200 comments/questions.

- Throughout the effort, institutions and individuals who are part of the research community also shared comments on the process and potential new models via an online portal, which has informed the conversations and work of the SME team.

- After developing two preliminary model proposals, the JAG hosted two additional public convenings in June to detail the options and take More than 2,000 individuals participated in each convening, with more than 800 comments/questions submitted.

- Subsequently, research institutions analyzed these provisional models and provided feedback (more than 175 responses) to the JAG to inform the final proposed

5. Will federal policymakers accept the FAIR model the JAG has proposed?

JAG organizations engaged congressional leaders throughout this process and seek to advance a new model that both meets the needs of the research community and addresses key concerns that members of Congress have expressed. Based on feedback the research community received from congressional engagements, we know there is an appetite for changing the manner in which indirect costs are determined. JAG organizations are engaging appropriate committees to inform them of the FAIR model and have proposed legislative language to implement it.

Working with congressional appropriations leaders, the research community helped to secure language in four appropriations bills and report language in five bills that blocks action on indirect costs in FY26. This language allows the research community more time to work with Congress and the executive branch to advance the FAIR model recommendations in FY27.

6. Which federal agencies should be required to use the FAIR model JAG has proposed?

In keeping with the current system of accounting and cost standards as delimited by the OMB Uniform Guidance (2 CFR Part 200), for the FAIR model to be effective and limit additional administrative burden, it should be adopted by all federal research agencies. Exceptions to the policy must be avoided. A transition period of two years should be implemented for institutions and government agencies to prepare their systems, policies, and practices for full adoption of the FAIR model.

7. Why does the FAIR model need to be adopted government-wide?

Research institutions and organizations often manage hundreds of federal awards from multiple agencies. A single set of indirect cost accounting rules under OMB Uniform Guidance (2 CFR Part 200) ensures that institutions do not have to maintain multiple, conflicting accounting systems to address variance in agency rules. This minimizes administrative overhead and allows more federal dollars to support actual research rather than accounting and compliance costs. Maintaining one set of rules under OMB Uniform Guidance is essential to ensuring consistency across agencies, reducing administrative burden, promoting fairness and transparency, and maximizing the impact of federal research investments.

8. How is the FAIR model more like how private foundations currently account for direct and indirect costs?

In developing the FAIR model, elements of existing models were examined including how private foundations account for direct and indirect research project costs compared to the current F&A system. The FAIR model adopts elements of the private foundation structure by moving more items into direct costing categories, making these costs more visible and explicit. Implementing these changes will require updates to the OMB Uniform Guidance (2 CFR Part 200) to allow for more direct charging.

9. How does the FAIR model impact the cost of a federal research grant?

The goal of the JAG effort was to develop a new model for funding the actual costs of supporting the performance of research in a fully transparent and accountable manner. The question of how much of that support should be divided between government sponsors and funding recipients is a separate issue, beyond the scope of the JAG effort. However, the FAIR model facilitates addressing this issue because it brings to light the actual costs of performing research. Institutions will continue to request no more than their cost of performing research.

10. How does the FAIR model ensure accountability and provide transparency?

Whereas the previous F&A model had transparency and accountability measures in the indirect rate proposal and negotiated rate process, the FAIR model requires additional accounting by universities to more clearly demonstrate that funds provided for General Research Operations (GRO) are appropriately spent. Further, rather than treating every research project the same irrespective of scope or nature of the research project support needs, the FAIR model specifically accounts for such differences, providing a common-sense approach to allocation of research support costs. In this way, the FAIR model provides greater accountability and transparency for the American taxpayer (as well as to researchers, administrators, and the federal government) about the true costs of federally sponsored research by allowing former indirect costs to be directly attributed and charged to specific research projects. Institutions will continue to follow federal regulations that require accountability and be subject to audits that verify accountability.

11. How does the FAIR model ensure accuracy of research costs?

The FAIR model ensures the accuracy of research costs by using more explicit line items to tie funding for specific research support activities, such as compliance costs and research facilities, to specific research project needs. This sustains recognition of regional cost differences by allowing charges for facility expenses (e.g. building and equipment depreciation, utilities, etc.) at actual cost. Linking costs directly to the characteristics of each research project allows for more precise and context-appropriate cost estimates, budgeting, and accounting. By using long-established tools such as intermediate cost objectives (for example, recharge/service centers) and the space survey already employed in current rate negotiations, institutions that perform research can map specific research requirements to the facilities and services each project requires.

12. How does the FAIR model address efficiency?

The FAIR model clarifies how indirect cost rates are determined, why they differ from one institution to the next, and how they translate to the actual dollar amount of total grant funding devoted to indirect costs. The model also recommends updates to the OMB Uniform Guidance (2 CFR Part 200) to require uniformity in agency policies – thereby eliminating agency-specific policies and requirements that cost both federal agencies and institutions additional time and funds. It also eliminates the current rate proposal and negotiation process – saving time and resources for both the federal government and institutions – and shifts focus to greater accounting of individual research project costs. The FAIR model creates potential efficiencies for both institutions and the federal government by reducing complexity for institutions that elect to use the “simple option.” By adding greater visibility into costs for facilities and administration, the FAIR model also incentivizes efficient use of research space and clarifies the costs of compliance and regulatory requirements.

13. How does the FAIR model reduce the administrative burden for both institutions and the federal government?

JAG acknowledges that there will be potentially significant upfront staffing and other costs required for some institutions to change systems that will not reduce administrative costs in the short term. However, in the long run, the new system eliminates the intensive process of negotiating institution-wide indirect cost rates with specific federal oversight and accounting offices located at the DOD Office of Naval Research and the Department of Health and Human Services. This saves both institutions and federal offices time and money.

Additionally, the FAIR model provides two accounting options – an “detailed option” and “simple option” (similar to the long- and short-form tax options) that will simplify calculations, particularly for small or emerging research institutions that may not have the administrative resources, or perform the types of research necessary, to complete the more detailed expanded version. Regardless of option, accountability and transparency measures are ensured through the FAIR model.

14. What institutions are most likely to adopt the “simple option” of the FAIR model?

The “simple option” is designed particularly for small and emerging research institutions that do not have the administrative resources to benefit from using the “detailed option.” However, R2 and R1 institutions may find the “simple option” attractive when the allocation of research support costs does not vary substantially between the types of research performed at the institution. The choice will be guided by an institution’s own analyses. An institution could also start out with the “simple option” and plan for the “detailed option” in the future when its research portfolio diversifies or it has more administrative resources.

15. Does an institution choose either the “detailed option” or the “simple option” of the FAIR model for the entirety of its research portfolio, or can it use one option for some funding agencies and another for others?

A determination must be made by the institution to adopt the “detailed option” or the “simple option” for all agencies. Mixing and matching would create incredible complexity for institutions as well as agencies. However, an institution may choose the “simple option” based on its current research portfolio and over time evolve to the more complex “detailed option” as its research portfolio changes. This will require a periodic review/adjustment period to be established and subject to further development.

16. Would universities continue to contribute their own funds towards research?

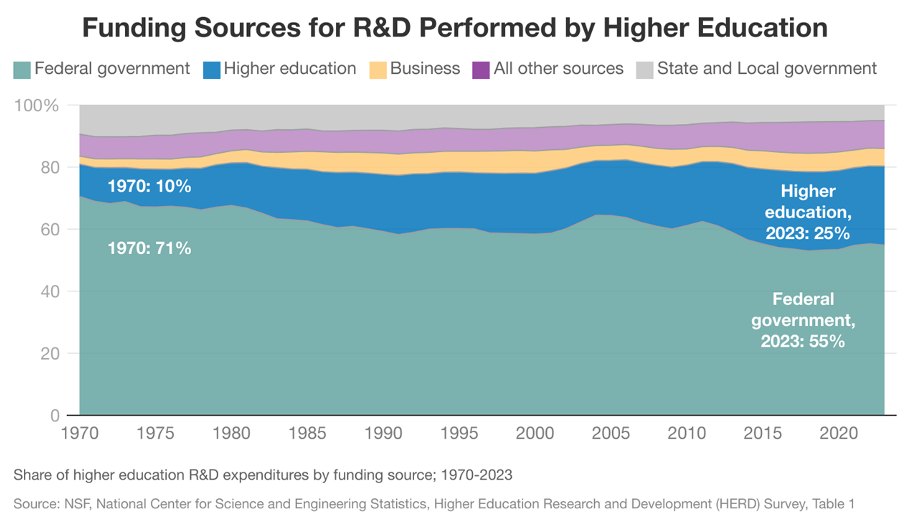

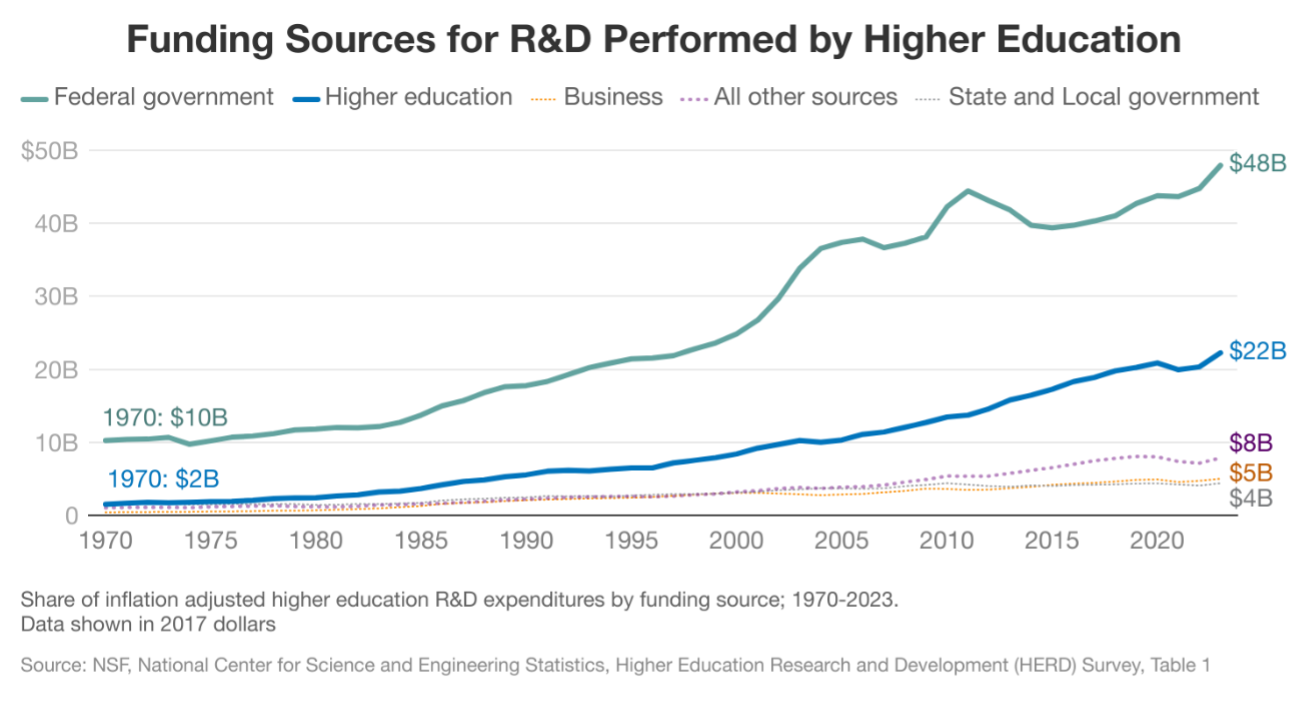

Yes, and they already contribute significantly under the current model. Behind only the federal government, universities are the second leading sponsor of the academic research and development (R&D) that take place on their campuses. Federal data show that colleges and universities pay for 25% of total academic R&D expenditures from their own funds. In FY23, this institutional contribution to pay for the R&D they perform amounted to $27.7 billion, including $6.8 billion in unreimbursed F&A costs. These institutional commitments to R&D significantly exceed the combined total of all other non-federal sources of support for academic R&D: state and local government (5%), industry [businesses] (6%), and foundation [other non-profit organizations] (6%) support in FY23. While the FAIR model addresses the unsustainable growth of research institutions’ contributions, colleges and universities will continue to financially support a significant share of the research they perform.

17. How does the FAIR model compare to a 15% cap on indirect costs proposed by NIH, NSF, DOE, and DOD?

The FAIR model provides a feasible alternative to both the existing F&A model and to the 15 percent cap on the F&A rate proposed by the NIH, NSF, DOE and DOD. Compared to an arbitrary, across-the-board 15% cap, the FAIR model will ensure that essential costs required to perform research are reasonably compensated, ensuring that institutions can continue to support research. While the accounting for these costs is calculated differently, these same costs are paid by the government to support government research at national laboratories, FFRDCs, and for-profit companies. Meanwhile, an arbitrary 15% cap fails to provide sufficient coverage of essential research costs for any research program. The FAIR model will also enable our country to continue leading the world in research and innovation while upholding the highest standards of ethics and accountability to American taxpayers. An arbitrary 15% cap is a cut to research and would mean fewer scientific innovations and breakthroughs for the American people.

Body

Transitioning to the FAIR Model

18. How long will it take to fully implement and transition to a new model? What is the proposed effective date?

Recognizing the complexity of shifting from the traditional F&A model to the FAIR model, sufficient time—two years—is needed for institutions and the government to prepare their systems, policies, and practices for full adoption. This approach would support institutional readiness, reduce disruption, and provide federal agencies with time to issue necessary guidance and updates to internal procedures.

A defined transition period ensures fairness, minimizes administrative disruption, and increases the likelihood of successful long-term adoption of the FAIR model. Once the transition concludes, all participating agencies and institutions should fully align with FAIR requirements for budgeting, reimbursement, reporting, and auditing.

19. What changes are needed to existing federal policies, regulations, and laws to implement the FAIR model?

While the FAIR model offers a structured, transparent, and auditable approach to funding federally sponsored research, its success depends on more than institutional adoption. The federal government must also implement a set of coordinated policy changes (starting with the OMB Uniform Guidance, 2 CFR Part 200) to ensure the FAIR model can function as intended. These policy shifts, which can be mandated by federal law, are necessary to align cost structures, reduce administrative burden, and update outdated reimbursement caps and regulatory mandates. Without such changes, the benefits of FAIR will be limited, and the opportunity to modernize research funding practices will be lost. Additional changes to regulations and possibly laws also will be necessary.

20. What changes may be needed to university policies and procedures to adopt the FAIR model?

All institutions will need to make changes to policies and procedures including revised terminology, budget instructions, and accounting structures if the new FAIR model is adopted. More significant changes likely will be necessary for institutions selecting the “detailed option.”

21. After transitioning to the FAIR model, how will the government ensure that institutions are charging only allowable costs?

While institutions will no longer be required to develop F&A cost reimbursement rate proposals or negotiate these rates with the government, they will need to continue to document their costing calculations, including the composition of cost pools and rate bases and how costs were allocated to pools and excluded from charges directly or through any other rate. These, as well as processes to ensure proper allocation of the significantly different costs of supporting various types of research, will be subject to the federal Single Audit. Institutions should anticipate that the Single Audit compliance supplement will include minimal auditing requirements for the “simple option” and more rigorous requirements for the “detailed option.”

Body

Other Questions

22. Why does the federal government provide support for indirect costs?

Indirect costs, also referred to currently as F&A costs, are the essential institutional costs associated with conducting world-class research projects on behalf of the federal government. F&A expenses currently include the costs of building and maintaining state-of-the-art research facilities; providing essential utilities and upkeep; supporting secure data storage and high-speed data processing; complying with multiple federal research security, human subject protections, and environmental health and safety requirements; and much more.

The federal government funds a share of indirect costs so research institutions can provide scientists and researchers with the resources and support they need to drive breakthroughs in science, technology, and medicine – advancements that keep our nation globally competitive and improve the lives of all Americans.

23. What would a reduction of federal indirect cost reimbursements—such as the caps proposed by NIH, NSF, DOE, and DOD—mean for universities?

Cuts to indirect research costs are cuts to research. If the federal government cuts back on reimbursements for the indirect costs of research, it may result in one or more of the following:

- The inability of universities to accept research awards from, and conduct research on behalf of, the American people through their federal agencies.

- The deterioration of research facilities as the financial risk to build new facilities or maintain existing ones becomes too great to cover with institutional funds.

- The inability to sustain required support staff and infrastructure required to comply with government regulations including research security; this could threaten the health and safety of patients, researchers and students.

- A reduction in the pipeline of trained scientists and engineers in the workforce due to reduced research training opportunities at universities.

- An increase in tuition rates due to the financial strain placed on universities.

Bottom Line: If such cuts are made, they will reduce the amount of research universities and their scientists can conduct on behalf of the federal government to achieve key national goals to improve the health and welfare of the American people, grow the economy, and enhance our national security. The FAIR model seeks to improve transparency and accountability while avoiding such cuts and the accompanying devastating effects on research nationwide.

24. Do universities ‘profit’ from the indirect cost reimbursements they receive associated with federal research grants?

No, universities do not financially gain from their indirect cost recoveries. As defined by the federal government, these are reimbursements for costs incurred by universities in conducting research on behalf of the government; thus, it is impossible for the cost reimbursements to result in a profit. The FAIR model was intentionally designed to provide greater transparency to research costs and more clearly demonstrate to lawmakers, regulators, and taxpayers how funds are spent by institutions in supporting federal research projects. Like the current model, under the FAIR approach we expect that institutions will continue to need to make investments of their own to conduct federally funded research.

Body